Hello! Kiah here. Welcome to Fintech Takes Banking, my weekly newsletter where I highlight things I think are interesting or important for bankers and the surrounding environs.

This newsletter comes to you from CBA Live 2026 in San Diego (or more accurately, the airports I had to visit to traverse to San Diego). If you’re reading this on Tuesday, it’s my actual birthday! 🎂 That’s right, your girl is an Aries ♈️ who always tries to end her first quarter of the year on a high note.

|

|

|

Q1’26: The Calm Before the Storm?

|

The first quarter always seems to me to be relatively quiet, as long as a global pandemic doesn’t shut the economy down or a massive bank run doesn’t result in the second-largest bank failure in U.S. history. Of course, there was some giant geopolitical news and financial drama during the quarter, the impacts of which are still flowing through the economy. But banks seem spared from the brunt of it — in the first quarter at least.

Nevertheless, the first three months of the year have passed at a dizzying pace. It can be difficult to remember the biggest, broadest takeaways for the banking industry during the quarter and compare them to the thematic throughlines that we’ve been tracking since the start of the second presidency of Donald Trump. So let’s dive into the quarterly recap.

|

How is the banking industry doing?

|

The banking industry ended 2025 with “strong earnings” aided by accelerated loan and deposit growth, according to the Federal Deposit Insurance Corp.’s quarterly banking profile. Net income for the year was up 10.2% from 2024, to $295.6 billion, driven by higher net and noninterest income, and the full-year return on assets was 1.2%.

The industry reported a fourth-quarter ROA of 1.24%, down 3 basis points from the prior quarter but up 13 basis points from a year prior. But community banks’ quarterly net income of $7.9 billion fell 3.8% quarter over quarter, due to higher noninterest expense and higher securities losses. Net charge-offs for the fourth quarter hit 0.63%, which was 15 basis points higher than the pre-pandemic average of 0.48%. However, the overall past-due and nonaccrual rate remained below pre-pandemic averages.

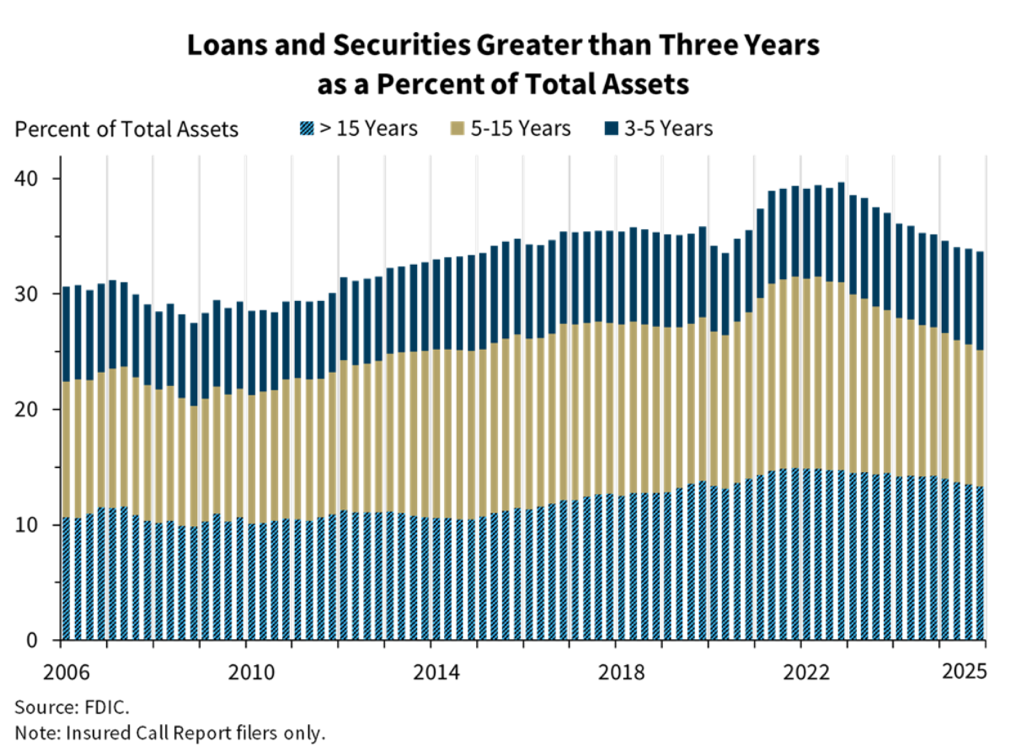

The FDIC also tracks the share of longer-term assets to total assets at banks, the percentage of which has fallen 12 quarters in a row and totaled 33.7% in the fourth quarter. This is the lowest level since 2020, and down from the peak of 39.7% three years prior. Longer-term assets still make up a larger share of community banks’ total assets: 42.9% at the end of 2025.

|

The number of problem banks, which had a CAMELS composite rating of 4 or 5, rose by a net three institutions during the quarter and totaled 60 by the end of the year. No banks failed during the fourth quarter, and two failed during the year. I wrote a little bit about the strange circumstances around the failure of Pulaski State Bank here.

In January, regulators closed Chicago-based Metropolitan Bank and Trust, a $261 million asset bank, and entered into a purchase and assumption agreement with Detroit-based First Independence Bank to assume “substantially” all the deposits and $251 million of the assets. According to the Fintech Cowboys, the bank held its bonds entirely in its available-for-sale portfolio, and unrealized losses in the portfolio totaled $14 million, compared to less than $8 million of Tier 1 capital, according to its final call report.

|

Interest in federal bank charters or deposit insurance remains high, and banking agencies remain receptive to them, given approval activity. Outside the United States, Latin American digital bank Nubank received conditional approval from the Office of the Comptroller of the Currency, 121 days after submitting its applications. European digital bank bunq formally filed for a de novo banking license with the OCC in January. The firm already has a U.S. broker-dealer license. Revolut, a UK digital financial technology firm, followed in March.

Inside the United States, the FDIC approved Echelon Bank’s application for federal deposit insurance, allowing the proposed state nonmember bank to launch in Clearwater, Florida. The FDIC approved the deposit insurance applications for Ford Credit Bank, GM Financial Bank and Edward Jones Bank; all industrial loan companies are domiciled in Salt Lake City, Utah. Affirm Holdings submitted applications to establish an ILC in Nevada. I wrote about the ILC trend here.

Upstart Holdings applied for a national bank charter in March, a development that my colleague Alex Johnson wrote throws its existing partnerships with chartered financial institutions into question.

In February, the OCC also finalized its existing rule on national trust bank chartering, affirming that national trust banks can engage in non-fiduciary activities, including certain custody and safekeeping activities. This is not a moment too soon, considering the regulator has approved five applications for trust banks for digital asset firms and has nine more to consider, including World Liberty Financial, which has connections to the family of President Donald Trump and the United Arab Emirates.

|

An Unrelenting Amount of Fed Stuff

|

I don’t know why I expect every quarter to have fewer major headlines and updates coming out of the Federal Reserve Board and System; I have been proven to be too naïve two quarters in a row. The agency’s work remains important to the nation’s financial system and a focus of the president. As a result, its work is becoming increasingly politicized, either deliberately or unwillingly.

The Federal Reserve received grand jury subpoenas from the Department of Justice that threaten a criminal indictment relating to Chair Jerome Powell’s testimony last summer about the central bank’s building renovation project. In March, a federal judge blocked the subpoenas as pretextual, citing a “mountain of evidence” suggesting the government was trying to exert pressure on the chair, and ordered the case’s docket to be unsealed. Those unsealed proceedings revealed a top deputy to U.S. Attorney Jeanine Pirro said the agency “did not have evidence of wrongdoing in its criminal investigation of the Federal Reserve over the cost of its building renovations.” The Justice Department said it would appeal the judge’s decision; the Federal Reserve is “formally opposing” the DOJ’s effort to reinstate its subpoenas to the central bank.

The Federal Reserve Bank of Kansas City approved Kraken Financial for a limited-purpose account at the beginning of March. Kraken is a crypto exchange that has a Special Purpose Depository Institution charter from Wyoming. The Kansas City Fed said that Kraken is a Tier 3 entity and that its initial account term of one year “includes restrictions and limitations tailored” to its business model and risk profile. Individual reserve banks can approve account applications, regardless of an applicant’s tier. Citing confidential business information, the Kansas City Fed declined to “disclose specific information about account holders’ access to the range of Federal Reserve financial services.” An article in The Wall Street Journal stated it includes Fedwire access but doesn’t include payment of interest on reserves.

The move surprised many in the financial services industry, given that it was about a month after the Federal Reserve Board closed its comment period on the proposed narrow or “skinny” master accounts. Skinny master accounts were proposed in an October 2025 speech by Gov. Christopher Waller.

In January, the U.S. Supreme Court heard arguments in the Trump administration’s efforts to fire Gov. Lisa Cook. Cook won her initial case in September, which the administration appealed. The justices, including some who have supported the president’s power to remove other appointed positions, expressed concerns about how this action would impact central bank independence and whether the allegations were grounds for dismissal, according to a write-up in The New York Times. The paper said the justices may order additional proceedings to substantiate the administration’s claims. Both Cook and Powell attended the argument.

Also in January, President Donald Trump nominated Kevin Warsh to be the next chair of the Federal Reserve Board. Warsh served on the board between 2006-11; if confirmed, the board chair term would begin mid-May. The Wall Street Journal observed that the nomination came as the president publicly shared his preferences for the direction of interest rate movement. Warsh’s confirmation hearings could begin in April; the nomination has been opposed by Thom Tillis, a Republican Senator from North Carolina on the Banking Committee, who is waiting for the DOJ to resolve its investigation into Powell.

In its role as national rate setter, the Federal Open Market Committee opted to keep the federal funds rate steady in the range of 3.5% to 3.75%. The committee’s job has become more complicated in the wake of the U.S. hostilities in Iran and the impact on oil prices. At the March post-meeting conference, Chair Powell “emphasized how little room officials might have to ease,” according to The Wall Street Journal. Looking forward, the summary of economic projections showed 12 of 19 participants penciled in at least one cut in 2026, the same as December 2025. But some participants reduced the number of cuts in the year, and one participant modeled a rate increase in 2027.

|

How is the economy doing?

|

Gross domestic product during the fourth quarter of 2025 grew at an annual rate of 0.7%, according to recently revised figures from the Commerce Department, a dramatic revision from the already-low 1.4% pace the department had reported in its advance GDP report.

A confluence of factors drove the revision and tepid activity, according to an article from The Wall Street Journal: slower consumer spending and business investment than initially reported, lower international trade activity and greater-than-reported government spending.

The unemployment rate hit 4.4% in February. Heather Long, chief economist at Navy Federal Credit Union, called the February jobs report “dismal” on Twitter and pointed out that the “US economy has LOST jobs since April 2025. Total job gains since May 2025 to February 2026 are now -19,000.” Long joined Bank Nerd Corner this quarter to discuss labor trends, including the K-shaped recovery.

|

The Federal Reserve, the Office of the Comptroller of the Currency and the Federal Deposit Insurance Corp. proposed a new set of capital rules in March that would lower capital requirements for a swath of banks, with a stated purpose of spurring lending.

The proposed rules would reduce aggregate capital requirements by about 8% for banks with less than $100 billion in assets and roughly 5% for the largest and most complex institutions when combined with other reforms, according to S&P Global. The proposal would lower capital requirements associated with a variety of asset types, including mortgages and consumer loans, along with favorable adjustments to the operations risk calculation that would impact wealth management, trust activities and credit card operations within depositories.

The rule could also allow banks to lower the capital they need to allocate to nonbank lenders, according to The Wall Street Journal. Some of these assets could be treated as securitizations, and this category could see a potential reduction of risk weighting if certain conditions are met. This approach comes as private credit is facing a redemption rush from investors who feel uneasy about their capital being locked up in loans following reports of fraud or firms facing a weakening financial outlook.

|

|

|

|